Higher education is important, and there shouldn’t be any barriers to getting it. And it doesn’t matter, even if you have to get a student loan.

After getting a higher education, you can also get a high-paying job and build a better future.

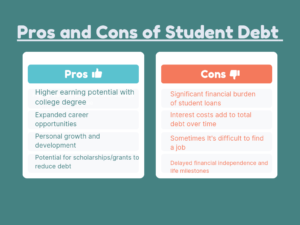

But the concerning thing is, do most students who take loans find the right job? And Is student loan debt worth it or not?

Understanding Student Debt

In 2021, A study conducted by the Federal Reserve shows that an average student is under $30,000 in debt. However, it’s just an average; many graduates have over $100,000 in student debt.

According to Federal Student Aid, undergraduates pay around 6.53 percent, graduate or professional students pay 8.08%, and parents and graduate or professional students pay 9.08% in interest.

Private student loans are normally higher than Federal Student loans. The average rate of student interest is around 4 percent to 17 percent, but it depends on the lender or the borrower’s creditworthiness, as per the report by Bankrate.

If we talk about the repayment timeline, federal student loans can generally be paid within ten years. Sometimes, you can also extend income through payment plans.

On the other hand, private student loans have different repayment periods ranging from 5 to 20 years, depending on your loan terms.

Here are a few differences between federal and private student loans:

Federal student loans:

- It’s offered by the U.S. government and has fixed interest rates set by Congress

- The loan eligibility is dependent on your financial need and various other factors

- Federal loans also offer income-driven repayment plans and the potential for loan forgiveness.

Private student loans:

- These loans are usually offered by banks, Credit unions, and other private lenders

- How much interest you’ve to pay on a student loan depends on your creditworthiness

- They don’t offer flexible repayment options or forgiveness options like federal loan

Return on Investment (ROI) of a College Degree

Here’s some data that can help you figure out if student debt is worth it or not; let’s understand the return on investment of a college degree.

1. Earnings by Degree Level

According to a 2021 study conducted by the U.S. Bureau of Labor Statistics (BLS) shows the median weekly earnings:

- High school diploma: $938

- Bachelor’s degree: $1,305

- Master’s degree: $1,545

- Doctoral degree: $1,909

This data shows that students with higher degree levels generally have higher Incomes.

2. Earnings by Field of Study

Here’s another study by PayScale, which they conducted in 2021-2022. It has found that the highest-paying bachelor’s degrees include:

- Petroleum Engineering: $137,720 median mid-career salary

- Electrical Engineering: $124,380 median mid-career salary

- Computer Science: $120,000 median mid-career salary

These were a few higher-paying bachelor’s degrees. Now, have a look at some lower-paying bachelor’s degrees:

- Early Childhood Education: $49,100 median mid-career salary

- Counseling: $52,400 median mid-career salary

- Social Work: $53,800 median mid-career salary

3. Return on Investment (ROI)

A study by the National Center for Education Statistics (NCES) shows that the average cost for a bachelor’s degree, which includes tuition, fees, room, and board, is around $22,180 to $54,880 per year. But it also depends on the institution.

According to Georgetown University’s Center on Education and the Workforce, the median lifetime average earnings for a bachelor’s degree holder is nearly $2.8 million, which is quite high if we compare it to a high school graduate, which is $1.7 million.

The earning potential is higher with a Master’s degree, which is around $3.2 million. With a doctoral degree, it’s $4 million, and $4.7 million with a professional degree.

These stats show a significant return on investment for a college degree, as the increased lifetime earnings can offset the upfront costs.

4. Potential for Career Advancement

According to a study by the U.S. BUREAU OF LABOR STATISTICS (BLS), An official website of the United States government, the unemployment rate in 2021 was:

- High school diploma: 5.8%

- Bachelor’s degree: 3.5%

- Master’s degree: 3.0%

- Doctoral degree: 2.5%

However, as of recent data of 2024, the civilian unemployment rate in the United States is around 4.2%.

This means that student loans are worth it because if you have a higher degree, you have the chance to get a high-paying job. On the other hand, the unemployment rate is very low, just 4.2%, according to the U.S. BUREAU OF LABOR STATISTICS (BLS).

So, with a degree, you have opportunities for career advancement. If we consider these factors, then student loans are worth it; you’ll make a return on investment (ROI) if you pursue a college degree.

When is Student Debt Worth It?

Okay, now let’s discuss whether taking on student debt is worth it and if it might be a good financial decision. Here are four different scenarios when you need to consider taking on a student loan:

1. Degrees with High Earning Potential

Student debt is worthwhile if you’re pursuing degrees in fields like engineering, computer science, healthcare, business, etc., Because in these fields, you can get high-paying jobs; therefore, It justifies the student debt.

For example, according to a study by PayScale, the median mid-career salary for a computer science graduate is $120,000. However, It depends on your college or university, experience, and other things.

Here are a different universities and earning potential:

Harvard University

- Early Career Pay: $121,800

- Mid-Career Pay: $210,800

Columbia University in the City of New York

- Early Career Pay: $122,000

- Mid-Career Pay: $210,100

Massachusetts Institute of Technology

- Early Career Pay: $128,700

- Mid-Career Pay: $210,100

2. Careers with Steady Demand and Growth

The Bureau of Labor Statistics projected many of the fastest-growing careers with consistent job opportunities and potential for career advancement, including technology, software development, nursing, and many other healthcare specialties.

These stats by BLS show that students’ debt might be worthwhile.

3. Scholarships and Financial Aid

If you can secure generous scholarships, grants, or any other financial aid, the net cost of your degree will be low enough, which will surely justify the student debt.

This makes the investment more manageable and will increase the overall return on Investment (ROI).

4. Potential for Higher Lifetime Earnings

There are many degrees with higher upfront costs, but during the lifetime, your earnings will outweigh the student debt.

As I mentioned earlier, the Georgetown University Center on Education and the Workforce reported that the median lifetime is $2.8 million if you have a bachelor’s degree, while it’s less than $1.7 million for a high school graduate.

Therefore, taking on student debt can be a good financial decision because when you pursue a degree or career with high earnings potential, you’ll easily cover whatever you’ve paid to get that job.

However, it’s important to carefully evaluate the ROI when considering taking on student loans.

Tips for Minimizing Student Debt

Here are some important strategies. If you follow them, they’ll help you reduce your debt burden while in school or college.

1. Part-Time Jobs and Internships

To minimize your student debt, you can focus on side income or an internship that will cover your daily expenses and reduce the need for student loans.

Finding any early morning job or part-time overnight job if you have any work to do during the day might be a good choice. Besides this, you can also choose a side hustle to make an extra income. For example, many students prefer overnight call center jobs.

By doing these part-time jobs, you’re not just making extra money but also gaining work experience, which will eventually enhance your resume.

2. Maximize Financial Aid

There are many financial aid opportunities that may help you if you’re struggling with student debt.

For example, you can fill out the Free Application for Federal Student Aid (FAFSA) every year. It can help you get into work-study programs, etc, and reduce your financial burden.

Besides this, many colleges and universities have their own institutional aid, such as grants, scholarships, and loan forgiveness programs.

However, if you want to apply for private scholarships and grants, make sure to do your research properly because they come from many different sources: private foundations, community organizations, professional associations, etc.

Besides this, you can consider exploring loan repayment assistance programs that will help you manage your student debt.

These were a few ways to maximize your financial aid as a struggling student with debt.

3. Live Frugally

As a student, when you’re dealing with student debt, living frugally is the first thing you’ve to do to manage your finances.

For example, you can create a detailed budget to track your income and expenses. You can identify areas where you can cut back, such as you can reduce grocery costs by 90 percent and save money on groceries.

You can also reduce discretionary spending on entertainment, dining out, or impulse purchases; there are around 250 ways to save money on everything and live frugally.

Moreover, as students struggle with debt, they can get cheap houses for rent, use public transportation, and buy used textbooks instead of new ones.

Take advantage of any discounts available to students, such as student discounts on software, subscriptions, or transportation. If you have a credit card, you can learn how to maximize your credit card rewards.

By earning extra income and living frugally, you can make additional repayments to your student debt.

Strategies for Managing Debt After Graduation

Here are three strategies for managing student debt after graduation:

1. Income-Driven Repayment Plans

If you want to manage your student debt after graduation, then you should consider enrolling in an income-driven repayment (IDR) plan. This plan is offered by the federal government based on your monthly loan payments and your income rather than the total amount of your debt.

An income-driven repayment (IDR) plan will provide you significant relief, as you’ll pay a few percent of your income, typically between 10-15%.

Another good thing about the IDR plan is that it offers loan forgiveness if you consistently pay for 20-25, but it depends on the specific plan.

The IDR plan makes it easy to tackle your student loans while managing other financial priorities, such as saving money for the future on a tight budget or building an emergency fund.

2. Consolidation and Refinancing

Another way to manage student debt after graduation is consolidation and refinancing.

- Consolidation: It combines multiple student loans into a single, new loan, which often has a fixed interest rate. You’ll repay this in a single month, which will reduce the overall interest rate.

- Refinancing: This way, you can replace your existing student loans with a new loan, and the interest rate is reduced. So, it’ll save over the life of the loan, as you’ll be paying less in interest.

Consolidation and refinancing are both beneficial for students in debt, but you need to have a strong credit profile and increase your income.

When considering consolidation or refinancing, make sure to read the terms and conditions of the new loan, such as interest rate, repayment period, or any fees associated with any of these processes.

Also, keep in mind that by refinancing federal student loans, you may lose access to a few things, such as income-driven repayment plans (IDR), loan forgiveness programs, etc.

Although by considering refinancing and consolidation, you make it easy to repay your student loan, make sure to compare offers from multiple lenders.

3. Prioritize Debt Repayment

You need to prioritize debt repayment to manage student loans after graduation so that you can create a structured plan to allocate your available funds and pay off your student debt fast.

Here are a few tips that can help you with that:

- Make a list of all your outstanding loans, including interest rates, minimum monthly payments, and balances.

- Pay the highest-interest loan first.

- You can also make an additional payment for the highest-interest loans because it’s the one costing you the most in the long run.

If you’re targeting high-interest loans, first make sure to increase your monthly debt payments. Side hustles or part-time jobs are excellent sources to earn extra income.

Consistently increasing your monthly payments will have a significant impact on the overall interest paid.

Besides this, don’t take any other new loan during the student or any other high-interest repayment process. Staying focused on the first debt and discipline is highly important.

Is Graduate School Worth the Extra Debt?

Yes! Pursuing graduate school is worth the extra debt and the reason is that you’ll get an advanced degree and develop specialized knowledge and skills, which will eventually open new career opportunities where you can earn a high income and repay all your debt.

However, keep in mind that this extra cost of graduate school will increase your overall student loan burden.

But we can say graduate school is worth extra debt because you’ll get benefits in the long term with a graduate degree while facing short-term financial strain.

A graduate degree will increase your potential salary depending on the field you’ve chosen, job prospects, etc.

Now you can decide whether you should attend a graduate school or not. But make sure to do a comprehensive analysis of your personal and professional goals, be realistic, and know your capacity to manage the extra debt.

Conclusion

Overall, taking on student loans is worth it because, with that money, you can get a higher degree, which means you’ll potentially increase your income by getting a high-paying job.

The ROI (Return On Investment) is pretty good. However, make sure to live frugally and get a side hustle or a job for extra money, which will help you pay your student debt.

{kind=link}

{kind=link}

{kind=link}

{kind=link}